Buy Now or Wait? How to Navigate the Property Market as Interest Rates Fall

Key takeaways

The RBA is Cautious, You Should be Decisive: Rates are easing, but slowly. The RBA’s data-dependent stance means a return to ultra-low rates isn’t on the cards. Waiting for massive cuts is a losing strategy.

Cheaper Credit Pushes Quality Assets Further Away: Lower rates increase borrowing power across the market. With listings for A-grade properties already tight, this simply means more competition and upward pressure on the prices of the very assets you want to own.

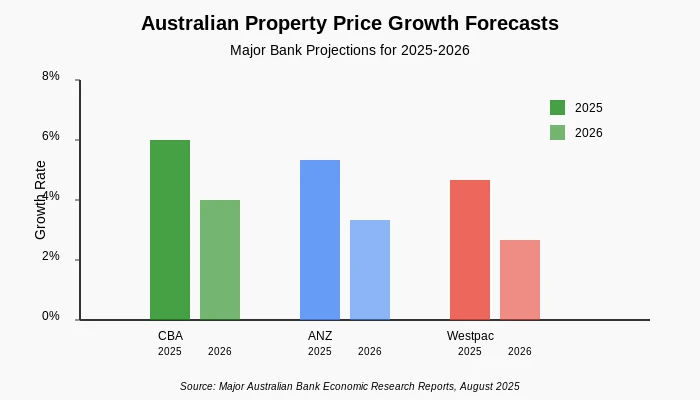

The Banks See Growth, Not a Bust: The mainstream forecast from banks like CBA is for national prices to keep rising, perhaps by 6% in 2025 and another 4% in 2026. If they’re right, waiting will cost you far more in capital growth than you’d save on interest.

It’s Always Quality Over Timing: This is the golden rule. The financial advantage of securing an A-grade asset at today’s price will almost always outweigh the marginal benefit of a slightly lower interest rate next year.

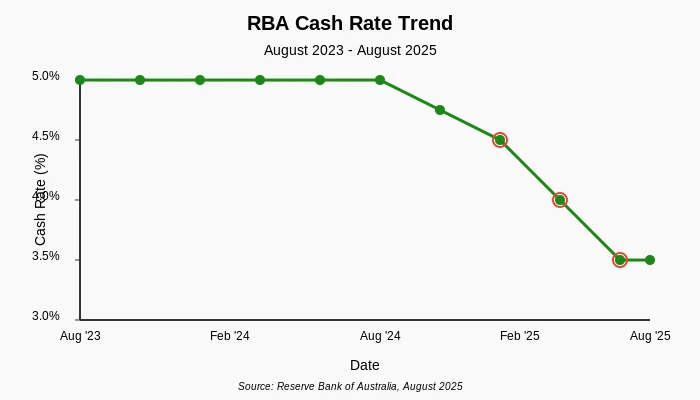

With the Reserve Bank finally starting to ease monetary policy, I’m getting a flood of calls from homebuyers and investors. The RBA has now cut the cash rate three times in 2025, bringing it down to 3.60%. And with every cut, the same question comes up:

“Jayden, should I buy now or wait for rates to fall even further?”

As a mortgage broker at Hunter Galloway, I see the logic. Cheaper repayments feel good, and a higher borrowing capacity is always welcome. But from my vantage point of seeing hundreds of property-buying journeys unfold, I can tell you this is often the wrong question to be asking.

Note: Focusing too much on timing the interest rate cycle is a classic mistake that can leave you worse off.

Successful, long-term property investors understand a crucial truth: you don’t time the market; you prepare to act when you find the right asset. Your finance strategy shouldn’t be about chasing an extra 25 basis point cut. It should be about getting yourself ready to buy a high-quality, investment-grade property that will grow in value for decades to come.

Let’s break down the strategic way to think about your finances in this new environment.

Figure 1: Major banks project continued property price growth through 2025-2026, with CBA forecasting 6% growth in 2025

The Unbreakable Link Between Credit and Prices

There’s a fundamental reason why waiting for lower rates can backfire: the price of the asset you want to buy doesn’t stand still.

Figure 2: The RBA has delivered three consecutive rate cuts in 2025, bringing the cash rate down to 3.60%

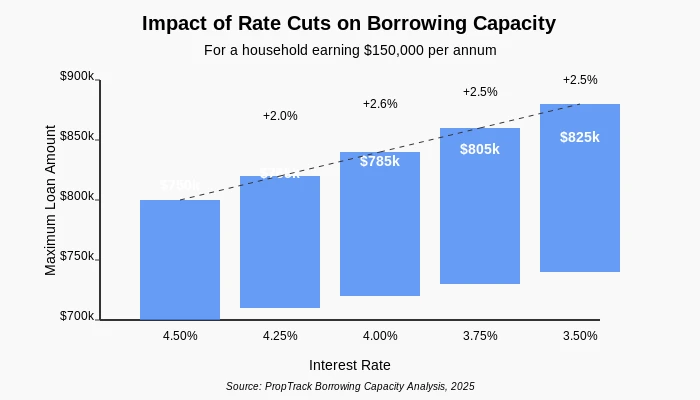

Lower interest rates make money cheaper. Cheaper money increases borrowing capacity. As PropTrack data suggests, even a single 0.25% cut can boost a typical buyer’s budget by around 2-3%.

Figure 3: Each 0.25% interest rate cut increases borrowing capacity by approximately 2-3%

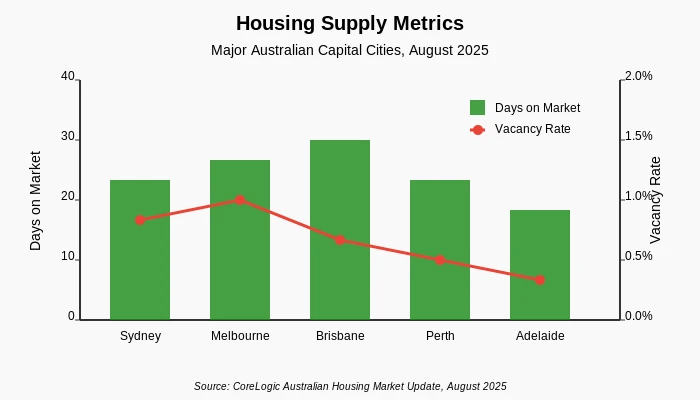

When that extra firepower meets a market with a low supply of quality homes for sale—which is exactly the situation in many of our capital cities—prices are inevitably forced upward. We’re already seeing this play out, with national values recording their sixth straight month of gains in July, according to Cotality.

Figure 4: Housing supply remains tight across major capital cities with low vacancy rates and decreasing days on market

This creates a dangerous illusion for those on the sidelines. You might feel prudent waiting for a cheaper mortgage, but the purchase price of the property you want is quietly drifting further out of reach.

The Real Cost of Waiting: A Worked Example

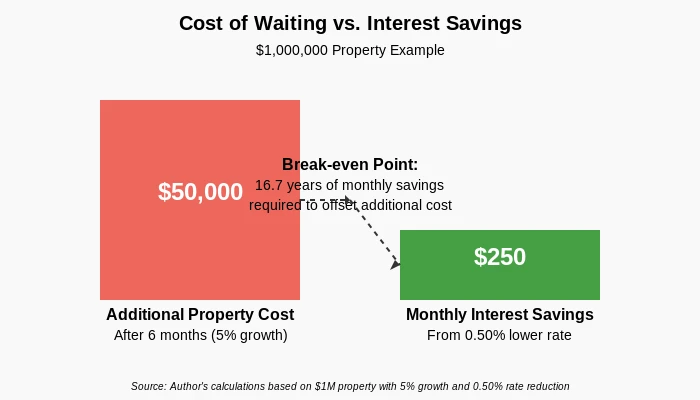

Let’s look at a simple scenario. Imagine you’ve found an investment-grade property for $1,000,000. You have your deposit, but you’re thinking of waiting six months in the hope the cash rate falls by another 0.50%.

- Risk of Waiting: The market moves by a modest 5% over that period (below the CBA’s forecast). The property you wanted is now priced at $1,050,000. You have to borrow an extra $50,000.

- The “Benefit” of Waiting: Your interest rate is 0.50% lower. On an $800,000 loan, this might save you around $250 per month in repayments.

Figure 5: It would take over 16 years of monthly interest savings to offset the higher purchase price after waiting just 6 months

The problem? You’ve paid $50,000 more for the asset to save a few hundred dollars a month on repayments. It would take over 15 years of those monthly savings just to break even on the higher purchase price you paid.

This is the trap. Buyers become so focused on the cost of the debt that they forget the far more powerful impact of the price of the asset. Seasoned investors know that paying less for a quality asset is the single most important financial lever you can pull.

The Strategic Buyer’s Finance Playbook for 2025

Instead of trying to time the RBA, a better approach is to control what you can. As a broker, this is what I advise my most successful clients to do.

Get “Investor Ready”

Before you even look at properties, get your financial house in order. This means having a stable income, a healthy emergency buffer (at least 3-6 months of living expenses), and a clear deposit strategy. Don’t be a spectator; be a prepared buyer ready to act.

Forge Your Finance Strategy

Don’t just get a loan; get the right loan structure. An offset account is non-negotiable for maximising your cash flow and reducing non-deductible debt. Consider a variable or split-rate loan to ensure you benefit from any future rate cuts. Most importantly, get a fully assessed pre-approval. A simple online calculator won’t cut it. You need the confidence of knowing the bank is ready to back you when you find the right property.

Asset Selection is Your North Star

Your finance is only as good as the asset it’s buying. This is the core of the Property Update philosophy, and from a finance perspective, I couldn’t agree more. Banks lend more willingly against quality properties in desirable locations because they represent a lower risk. Focus your search on A-grade homes or investment-grade properties with proven long-term performance and strong demographic drivers. Let this be your non-negotiable.

Read the Real Market Signals

Ignore the dramatic media headlines. Watch the leading indicators in the suburbs you’re targeting. Are days-on-market falling? Is vendor discounting shrinking? Is the number of new listings low? These are the real-time signs of rising competition and a market that won’t wait for you.

The Bottom Line

Trying to pick the bottom of the interest rate cycle is a seductive but ultimately distracting game. For serious homebuyers and investors, the playbook should be simple and disciplined.

If your finances are organised and you find an A-grade asset in an investment-grade location, the evidence suggests you should act. A conversation with a mortgage broker can help you take the next step with confidence.

In an environment of tight housing supply and easing rates, the cost of the asset rising will likely eclipse any small savings you might get from a lower rate in the future.

If you’re not financially ready, then wait—but wait with intent. Use the next few months to aggressively build your deposit, clear consumer debts, and work with a broker to get your loan strategy locked in.

The real edge isn’t found in guessing the RBA’s next move. It’s found in buying the right property with the right finance structure, and then letting time and compounding do the heavy lifting.